SECURE Act: How Changes to Retirement Accounts Could Affect your Estate Plan

SECURE Act: How Changes to Retirement Accounts Could Affect your Estate Plan

and

Notable Changes in Washington’s Real Estate Excise Tax Laws

On December 20, 2019, the SECURE Act (Setting Every Community Up for Retirement Enhancement Act of 2019) was signed into law. The SECURE Act made significant changes to the law governing IRAs (individual retirement accounts) and other types of qualified retirement and defined benefit pension plans, such as 401(k)s, 403(b)s, and 457(b)s (referred to together hereafter as “IRAs”). Most provisions of the law went into effect January 1, 2020. Important and positive changes from the Act include:

- The required minimum distribution age increased to 72, up from 70 ½, for individuals who reach age 70 ½ after December 31, 2019.

- Elimination of an age limit for making IRA contributions.

- New parents can take penalty-free withdrawals (up to $5,000 for each parent).

- Long-term part-time employees may now be eligible for participating in 401(k) plans.

From an estate planning perspective, the biggest change is that inherited IRAs must be distributed entirely within ten years. Prior to the Act, an individual who inherited an IRA could stretch out the withdrawals and required income tax payments based upon the inheriting individual’s life expectancy. However, under the Act, if the account holder dies after January 1, 2020, the beneficiaries of the inherited IRA must withdraw all of the assets by December 31st of the year that contains the 10th anniversary of the date of death (the “ten-year rule”).

The ten-year payout rule can have potentially negative and unforeseen tax and estate planning consequences. One very likely consequence is the acceleration and increase in income taxes paid by the beneficiary upon distribution of the IRA. But another, equally concerning consequence is that a young beneficiary may receive a large lump sum payment, rather than deferred or stretched out payments, contrary to the account owner’s wishes. This result could put a large retirement account in the hands of an imprudent beneficiary much sooner than anticipated.

The unintended acceleration of payouts might occur even if the IRA account is to be paid to a trust instead of a beneficiary directly. A common type of trust used to inherit IRA accounts is the “conduit” trust. This type of trust requires the trustee to pay out the required minimum distributions to the beneficiary immediately—which under the SECURE Act will mean the distribution of the entire IRA to the beneficiary via the conduit trust within ten years of the account holder’s death. Given this, account owners may want to consider using an “accumulation” trust rather than a “conduit” trust. Unlike a conduit trust, IRA distributions paid to an accumulation trust can be retained inside of the trust during and beyond the ten-year period, with discretionary rather than mandatory payments to the beneficiary as needed. An accumulation trust could help protect the beneficiary from squandering his or her inheritance, in addition to protecting the IRA distributions from a divorcing spouse, bankruptcy, or a creditor of the beneficiary.

Clients who have named a trust as a beneficiary of an IRA account should call their attorney at Karr Tuttle to review whether the trust is a conduit trust or an accumulation trust, and to discuss whether any updates or changes to their estate plan are needed at this time. In addition, clients who have named children or otherwise possibly imprudent individuals as direct beneficiaries should review their estate plan and consider whether the ten-year payout rule merits the use of an accumulation trust.

There are some notable exceptions to the ten-year rule. A spouse may still roll over a deceased spouse’s IRA and take a stretch pay out. If the beneficiary is a minor child of the account owner, the beneficiary may take the benefits over his or her life expectancy and upon attaining the age of majority (age 18 to 26, depending on the circumstances), the ten-year rule will apply. A disabled and chronically ill beneficiary (or a qualified trust for his or her benefit) may also avoid the ten-year rule. In addition, a beneficiary who is not more than ten years younger than the deceased owner/participant can use his or her life expectancy to calculate the required minimum distribution.

This alert only provides a brief overview of the SECURE Act. Please review your estate plan to determine how the Act impacts your plan and discuss any concerns with your attorney.

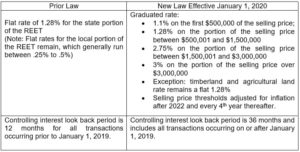

Also of interest are recent changes to Washington State’s real estate excise tax (REET) laws. In May 2019, the Washington legislature changed significant aspects of the REET which were made effective January 1, 2020. Some of the key changes are reflected in the following comparison table:

When a controlling interest in an entity holding real property is transferred for valuable consideration, REET applies to the value of all real property owned by the entity in Washington State without any deduction for mortgages, liens, or other debts. A controlling interest generally means 50% or more of the voting power or capital interest in the entity, and the transfer may be in a single transaction or series of transactions by one person or by a group of persons acting in concert. The new legislation requires all transfers that amount to at least one-third of a controlling interest (16.67%) in an entity that owns real estate in Washington to be reported to the Secretary of State so they may keep track of transfers within the now 36-month reporting period.

For the most part, the exclusions to the REET have not changed. Some examples of these exclusions include the following transfers of real estate or interests in entities holding real estate: gift (although the transfer of underlying debt is consideration and subject to REET); inheritance; community property and dissolution; irrevocable trusts; mere change in identity or form (e.g. transfer to an entity in return for a prorata interest); and entity formation or liquidation that does not involve the recognition of gain or loss for federal income tax purposes.

If you have questions regarding Washington’s Real Estate Excise Tax, please contact your Karr Tuttle Campbell attorney for more information and assistance.